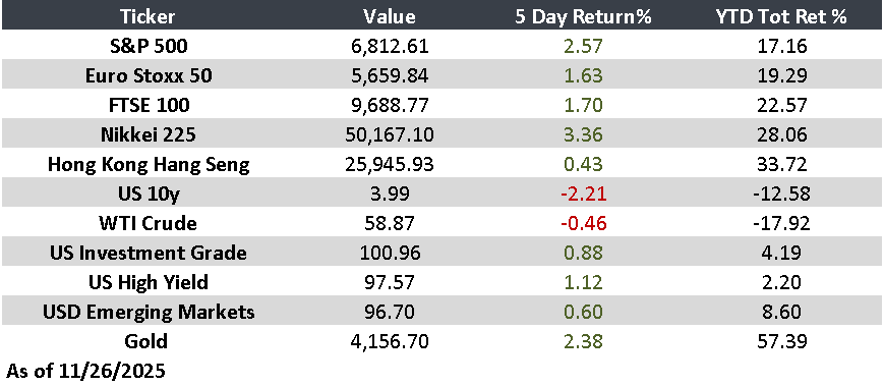

Week of June 1–5

Markets remain resilient despite inflationary pressures and global challenges

The global economy continues to display mixed signals. While the United States remains supported by strong employment and economic activity, Europe faces rising inflationary pressures and Asia presents a contrast between recovering demand and slowing industrial activity. Investors remain focused on the path of interest rates and the performance of corporate earnings.

United States

Markets pulled back after reaching record highs as bond yields moved higher. Employment and economic activity exceeded expectations, while investor appetite for AI and technology infrastructure companies remained strong.

Europe

Eurozone inflation reached 3.2%, driven by higher energy prices. Manufacturing continues to expand modestly, although elevated costs and softer new orders are weighing on momentum.

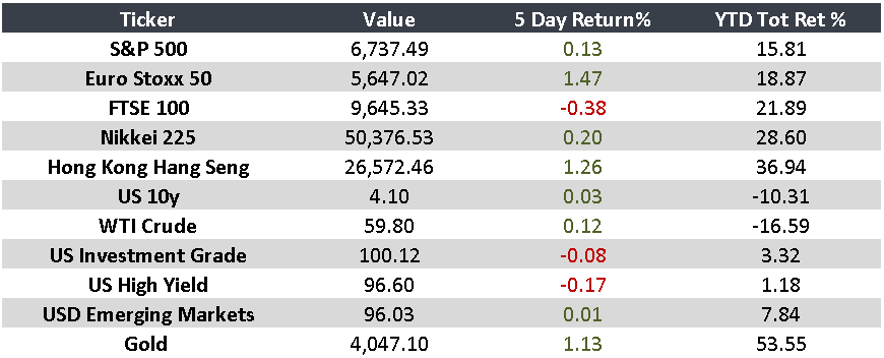

Japan

Manufacturing and services activity showed signs of slowing. Input costs continue to rise, while both domestic and external demand are gradually losing momentum.

China

Manufacturing growth moderated but exceeded expectations. Services activity posted its strongest performance since February, supported by improving domestic demand.

Argentina

The government will move forward with its application to join the CPTPP, reinforcing its trade liberalization strategy and deeper integration into global markets.

Brazil

Manufacturing activity contracted due to weaker demand and supply-chain disruptions. However, industrial production maintained solid year-over-year growth, highlighting the sector’s resilience.

Mexico

Lower tax revenues are increasing pressure on fiscal deficit targets. Meanwhile, remittances continue to grow, while fixed investment remains on a prolonged weak trend.

“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria.” — Sir John Templeton

KEY UPCOMING EVENTS

- In the United States, inflation data (CPI) will be released 06/10

- In the United States, PPI will be released 06/11

Monitor:

Note: Returns as of 10 AM ET.