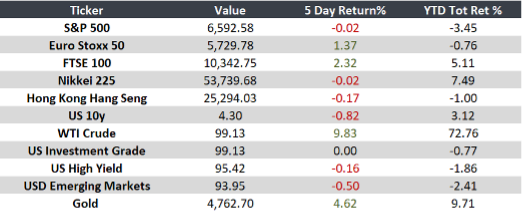

Week of March 30 to April 3 Inflation, energy dynamics, and mixed growth signals shaped global markets. Markets reflect a […]

Insights AWM

We share market analysis, economic outlooks, and insights on relevant financial topics prepared by our Investment Committee. This material is intended for informational purposes only and does not represent the views of any individual advisor.

Markets: Inflation, Oil, and Slowdown

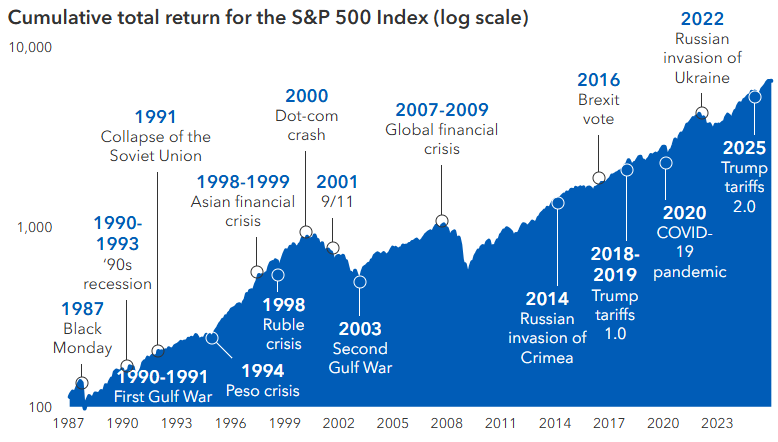

Volatility: Navigating Uncertain Markets

Discipline and perspective in times of uncertainty Periods of volatility are a natural part of markets. While they create uncertainty, […]

Global Outlook: Inflation, Rates, and Conflict

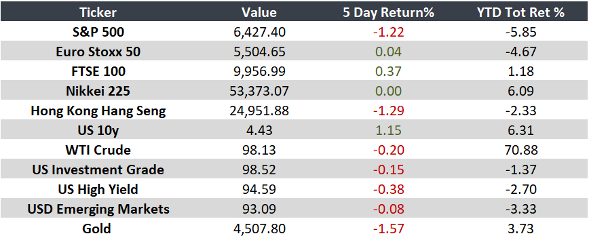

Week of March 23–27 Markets faced a week marked by geopolitical tensions and inflationary pressures. While the U.S. shows labor […]

Holistic Due Diligence Is a Must

Due diligence isn’t just about validating performance metrics or checking boxes on operational risk. In alternatives—where relationships are long-term, structures […]

Markets focused on inflation and geopolitical risks

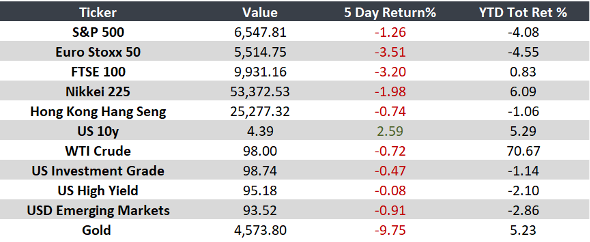

Week of March 16–20 Financial markets remained volatile amid ongoing inflationary pressures and geopolitical risks. Monetary policy decisions and economic […]

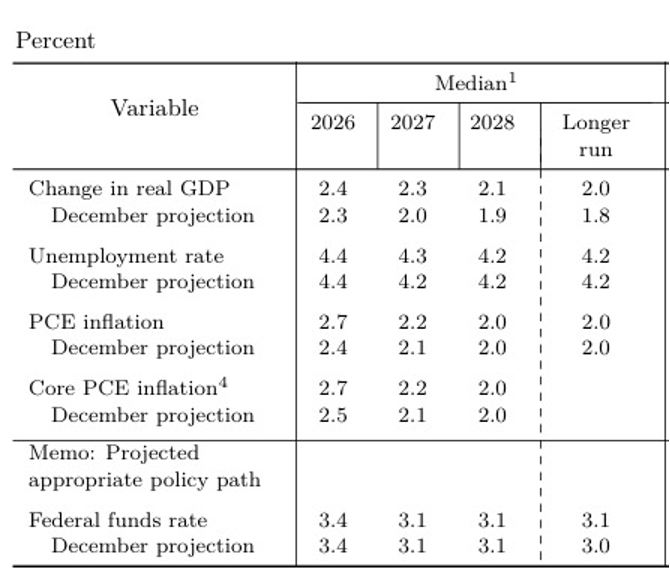

Fed Holds Rates Amid Uncertain Outlook

The Federal Reserve decided to keep its benchmark interest rate unchanged within a range of 3.5%–3.75%, amid persistent inflation, mixed […]