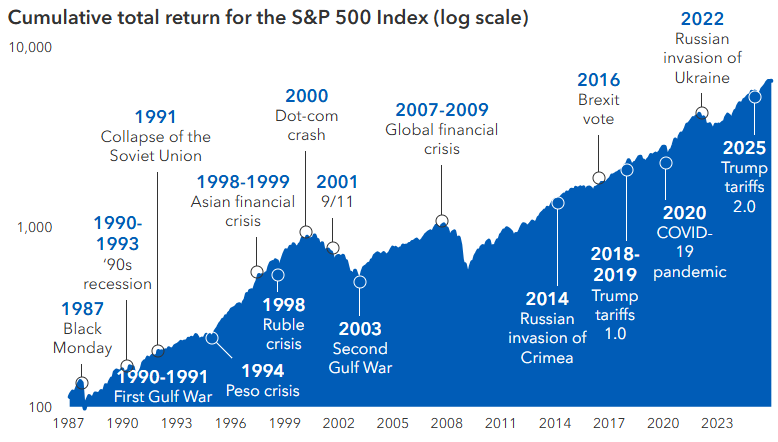

Discipline and perspective in times of uncertainty

Periods of volatility are a natural part of markets. While they create uncertainty, they also highlight the importance of maintaining discipline. In these environments, it is essential to recognize our reactions, put events into perspective, and stay focused on long-term objectives.

History shows that despite recurring crises, markets have remained resilient. Avoiding impulsive decisions and maintaining consistency in strategy often matters more than reacting to short-term movements.

Volatility can create opportunities, but it requires focus. Beyond short-term noise, it is a good time to revisit objectives, evaluate gradual adjustments, and consider strategies such as rebalancing or phased investing. In many cases, the best decision is to stay the course. Consistency, rather than market timing, has historically been the primary driver of long-term portfolio value.

Source: Capital Group, Standard & Poor’s