Market declines are part of investing; disciplined reactions can make the difference. Keys to staying on course when markets decline.

Perspective and Discipline During Volatility

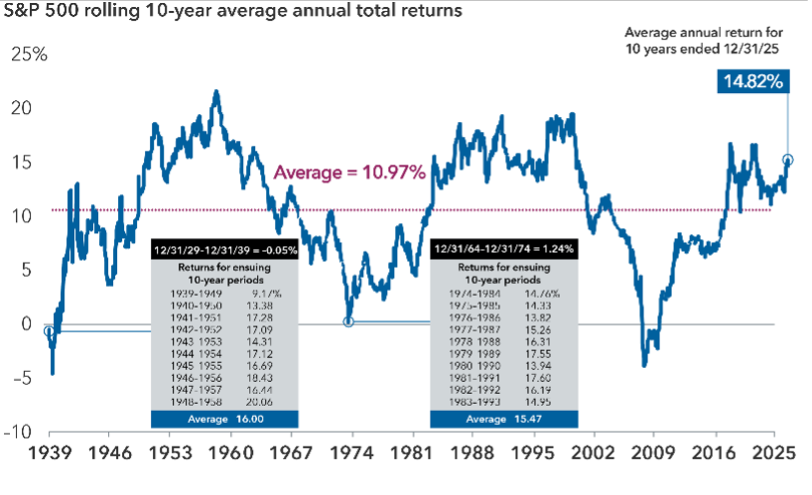

Market declines are inevitable and often lead to impulsive decisions. However, history shows that corrections have been temporary and followed by recoveries. Maintaining a defined strategy, diversifying, and avoiding attempts to anticipate every market move can help protect long-term goals. Rather than eliminating volatility, the challenge is to manage it with perspective and discipline.

Time in the market is often more important than finding the perfect entry point. Leaving the market may mean missing some of the strongest recovery days. A diversified portfolio, including fixed income and regular contributions, can reduce volatility and support more rational decisions. During downturns, staying committed to the plan is often more effective than reacting to market noise.

Monitor

Source: Capital Group, Morningstar, RIMES, S&P.