Week of March 30 to April 3

Inflation, energy dynamics, and mixed growth signals shaped global markets.

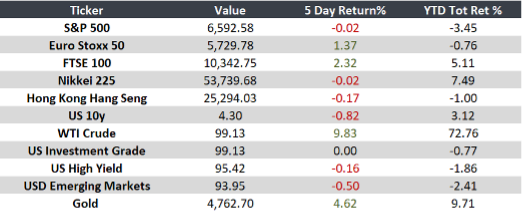

Markets reflect a complex environment, with inflationary pressures, geopolitical-driven volatility, and mixed growth signals. The U.S. remains resilient, while Europe faces higher costs and emerging markets show signs of slowdown.

United States

A quieter week, but with mixed signals: solid consumption, softer labor momentum, and rising cost pressures. Recession risk increases amid higher oil prices and tensions with Iran.

Europe

Inflation rises driven by energy and remains above the ECB target. Unemployment is stable, but job creation slows. The UK shows moderate growth.

Japan

Stable labor market, but weak consumption. Retail sales decline despite fiscal support, highlighting fragile domestic demand.

China

Manufacturing PMI improves, supported by public spending and AI demand, though input cost pressures remain elevated.

Argentina

Labor reform partially halted by court intervention, increasing regulatory uncertainty.

Brazil

Decline in producer prices suggests easing inflationary pressures ahead, supporting expectations of price stability.

Mexico

Banxico nears the end of its rate-cutting cycle. Risks persist from low growth and elevated inflation, with weak economic activity and exports.

“The two greatest enemies of the equity fund investor are expenses and emotions.” – Jhon Bogle

Key upcoming events

- In the United States, Manufacturing PMI will be released on 04/06

- In the United States, March inflation data will be released on 04/10

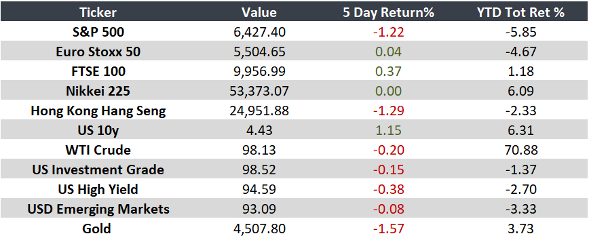

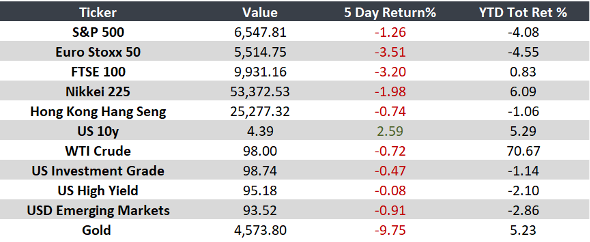

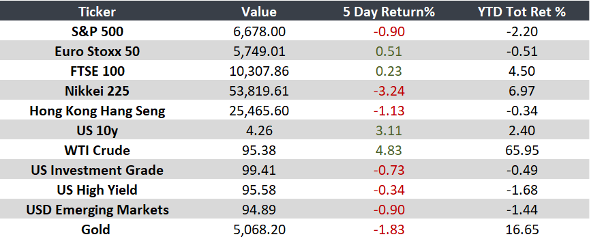

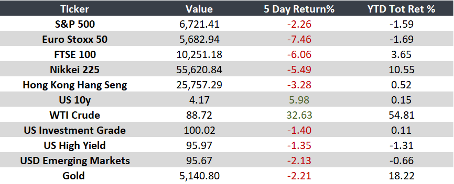

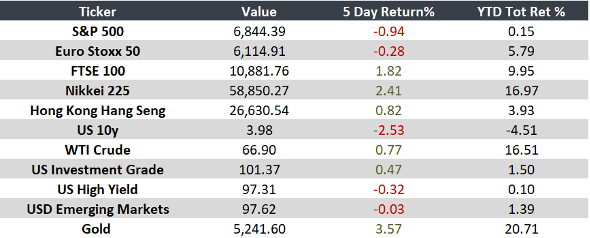

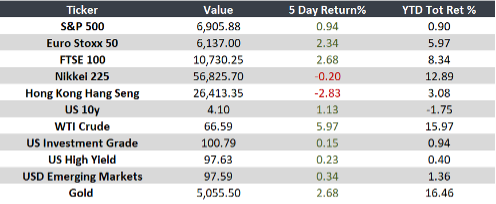

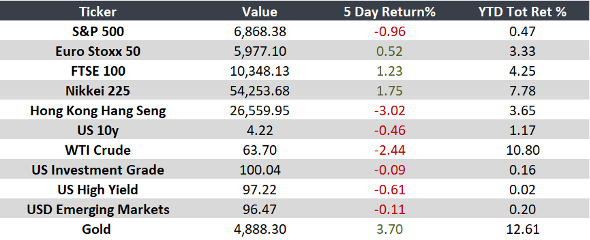

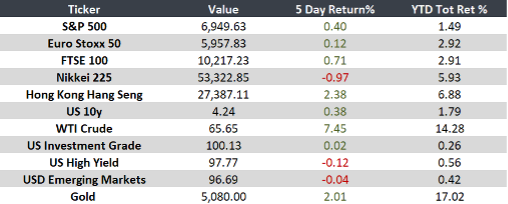

Monitor

Note: Short week due to festivities.