Week of July 13–17

Lower inflation, corporate earnings, and uneven growth signals shaped the week.

Markets assessed the start of earnings season alongside easing inflation in the United States. However, geopolitical tensions and weaker activity and investment continue to create an uneven global economic environment.

United States

- Inflation eased and the labor market remained resilient. Early corporate earnings exceeded expectations, although technology-sector volatility and geopolitical tensions weighed on markets.

Europe

- Eurozone inflation continued to decline, but industrial production remained weak. The United Kingdom posted moderate growth, supported by the services sector.

Japan

- Industrial production edged higher during the month but declined year over year due to weakness in machinery, pointing to a still-fragile recovery.

China

- GDP growth slowed due to weak consumer spending and lower investment. Exports rebounded strongly, supported by demand related to artificial intelligence.

Argentina

- Annual inflation increased, although the monthly pace moderated. Tourism, housing, and regulated services continued to drive price pressures.

Brazil

- Retail sales and the services sector posted limited growth. Weakness in transportation confirmed a moderate economic activity environment.

Mexico

- Formal employment and manufacturing payrolls continued to weaken, while private consumption remained resilient, supported by real wage growth, remittances, and low unemployment.

“Investing is the intersection of economics and psychology.”

— Phil Town

KEY UPCOMING EVENTS

- In the United States, employment related data will be released 07/21

- In the United States, manufacturing PMI will be released on 07/24

Monitor:

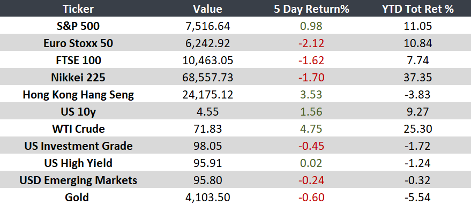

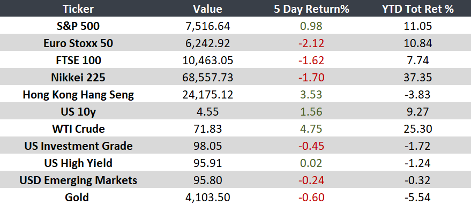

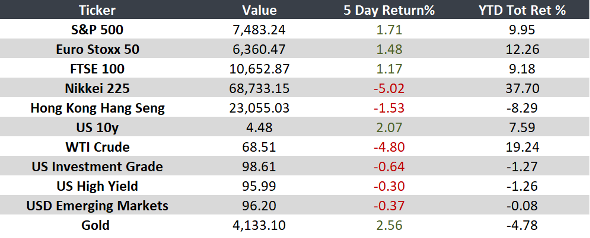

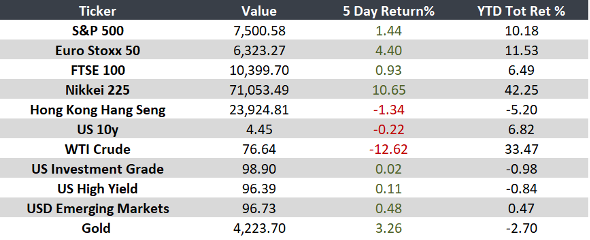

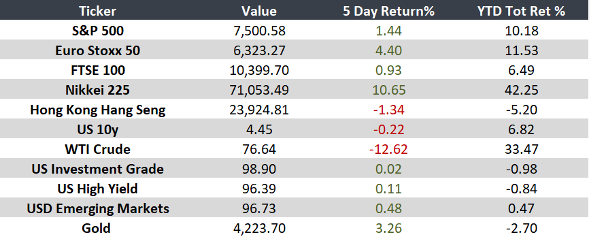

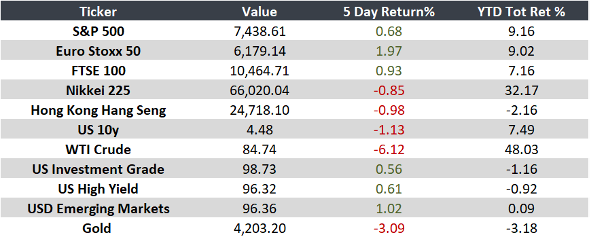

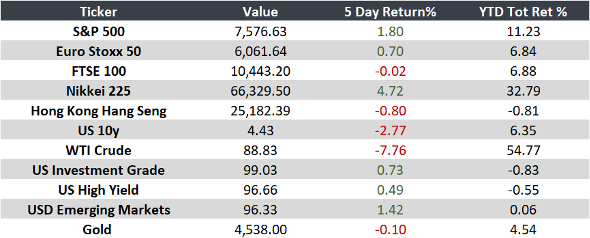

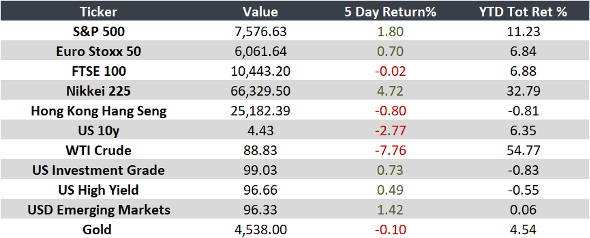

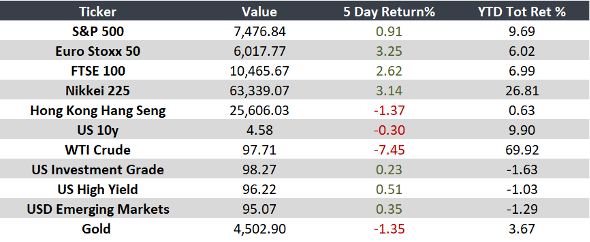

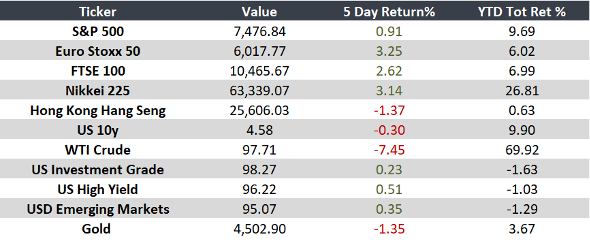

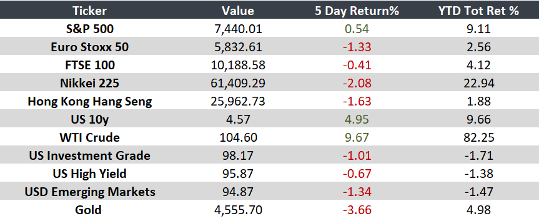

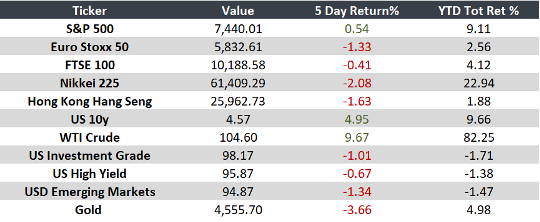

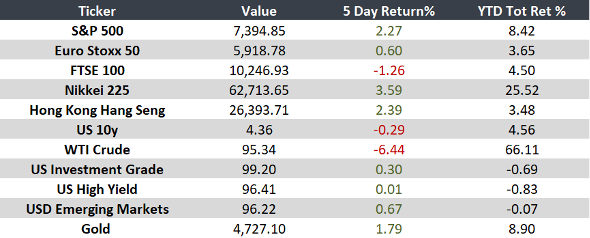

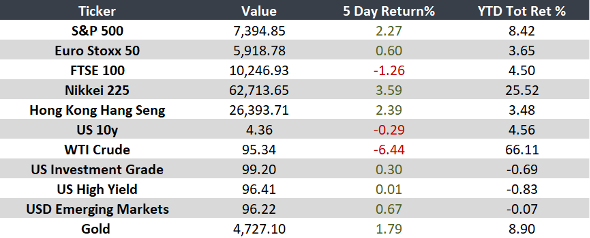

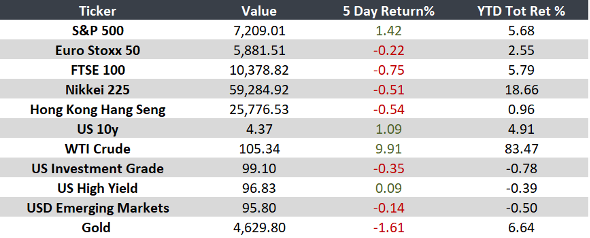

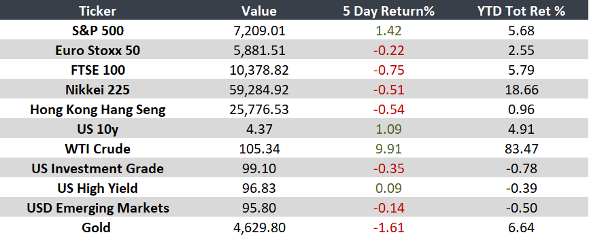

Note: Returns as of 10 AM ET.