Global Weekly Overview

Week of May 4 to May 8

A week marked by inflation pressures and slowing activity

Recent data point to a moderate growth environment with persistent cost pressures. Inflation driven by energy and geopolitical tensions continues to shape monetary policy decisions globally.

United States

- Strong earnings (83% beating estimates) drive profit growth to ~23%.

- Employment exceeds expectations but is slowing.

- PMI signals rising cost pressures that could pass through to inflation.

Europe

- Industrial costs remain elevated and services PMI drops to a 62-month low.

- In Germany, weakness in manufacturing and services increases recession risks.

Japan

- Services activity slows, while central bank minutes suggest potential rate hikes.

- Energy shocks are raising inflation risks and pressure on exports.

China

- Composite PMI improves on stronger demand, but input costs reach their highest levels since 2022, pressuring margins and growth sustainability.

Argentina

- Industrial activity rises 5.0% year-over-year, driven by chemicals. However, sectors such as machinery and textiles remain in contraction.

Brazil

- Industrial production rebounds 4.3%, reflecting the positive impact of rate cuts despite a more challenging global environment.

Mexico

- Banxico cuts rates to 6.50% and inflation slows.

- Investment falls 4.2%, signaling weaker momentum and pressure on future growth.

“Time is your friend, impulse is your enemy.” — John Bogle

KEY UPCOMING EVENTS

- In the United States, Inflation data will be released — 05/12

- In the United States, PPI data will be released — 05/13

Monitor:

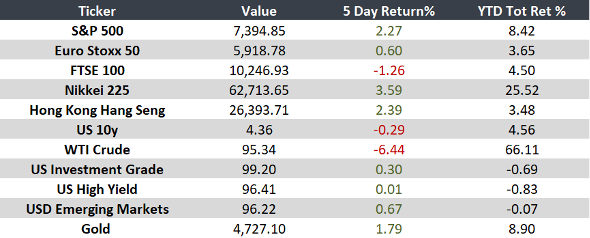

Note: Returns as of 10 AM ET.