Global Outlook: Inflation, Rates, and Conflict

Week of March 23–27

Markets faced a week marked by geopolitical tensions and inflationary pressures. While the U.S. shows labor market resilience, Europe and Japan present mixed signals, and emerging markets like Mexico face challenges in growth and inflation.

United States

Negotiations with Iran remain stalled despite a temporary truce. Manufacturing PMI hits an 11-month low; rising import prices reinforce expectations of higher-for-longer interest rates.

Europe

Manufacturing PMI improves, but the conflict increases costs and delays inputs. Business confidence declines amid uncertainty, particularly impacting the services sector.

Japan

Inflation falls below the BoJ target, but the central bank adopts a more hawkish tone amid inflation risks linked to a weaker yen and geopolitical tensions.

China

The semiconductor industry gains momentum driven by AI. It is projected to reach 41% of global capacity in key chips for autos and smartphones by 2028.

Argentina

Economic activity expands, supported by agriculture and fishing, offsetting weakness in industrial and commercial sectors.

Brazil

Consumer confidence improves, driven by better household financial expectations, though current conditions remain weak.

Mexico

Banxico cuts rates to 6.75% in a split decision. Inflation rises and economic activity declines, pointing to a slowdown with ongoing inflationary pressures.

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach.” – Peter Lynch

Key upcoming events

- In the United States, employment data will be released on 03/31

- In the United States, nonfarm payrolls will be released on 04/03

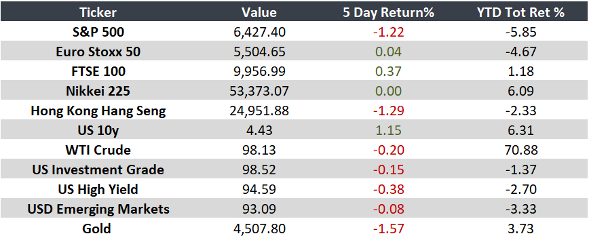

Monitor