Markets focused on inflation and geopolitical risks

Week of March 16–20

Financial markets remained volatile amid ongoing inflationary pressures and geopolitical risks. Monetary policy decisions and economic data continue to shape expectations for global growth.

United States

The Fed kept rates unchanged at 3.5%–3.75% amid persistent inflation and rising energy prices. It also eased bank capital rules, while the PPI surprised to the upside and jobless claims confirmed labor market strength.

Europe

Germany’s economic sentiment dropped sharply due to higher energy costs, although PPI declined on lower energy prices. The Bank of England held rates steady, while UK unemployment stabilized at elevated levels.

Japan

The Bank of Japan maintained its policy rate at 0.75% and warned of upside inflation risks linked to oil prices. Exports rose for a sixth consecutive month, though supply chain risks remain due to higher energy costs.

China

Industrial production expanded, supported by technology and shipbuilding sectors. However, the housing market remains weak, with declining prices and unemployment rising above expectations.

Argentina

Unemployment rose to 7.5% in Q4 2025, while consumer confidence fell to levels last seen in October, reflecting a challenging economic environment.

Brazil

The central bank cut rates to 14.75%, less than expected, citing inflationary and geopolitical risks. Industrial confidence declined amid high interest rates and global uncertainty.

Mexico

The Mexican Banking Association revised down expectations for rate cuts due to global inflation risks. GDP growth is projected at 1.5% in 2026, still below potential. Key US PMI and labor data will be released this week.

“Never invest in a business you cannot understand.” – Warren Buffett

Key upcoming events

- In the United States, Manufacturing PMI will be released on 03/24

- In the United States, employment data will be released on 03/26

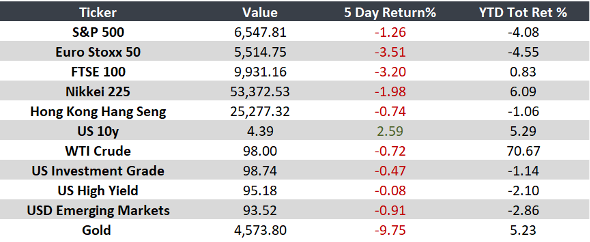

Monitor