Global Weekly Outlook

Week of July 6–10

Markets combined lower volatility with mixed signals on growth and inflation.

Markets remained relatively stable, although challenges related to inflation, international trade, and monetary policy persist. While the United States and Europe continue to show resilience across several indicators, Asia and Latin America face more specific economic headwinds.

United States

- Markets posted modest gains despite continued volatility in oil prices. The Fed remains firmly data-dependent, while the trade deficit widened and services activity continued to lose momentum.

Europe

- Consumer spending continues to recover and Germany’s external trade improved. However, higher producer prices indicate that inflationary pressures have not fully subsided.

Japan

- Producer price inflation remains elevated, although the monthly pace of increase moderated, suggesting a gradual easing in cost pressures.

China

- Consumer inflation continued to soften, while producer prices posted their strongest increase in several years, reflecting rising costs across the industrial sector.

Argentina

- The government is seeking to secure debt financing through domestic and multilateral sources, prioritizing lower borrowing costs before returning to international capital markets.

Brazil

- Inflation continued to moderate thanks to lower food and housing costs, although energy prices remain a significant source of inflationary pressure.

Mexico

- Inflation fell to its lowest level since 2020, while investment showed signs of recovery. However, uncertainty surrounding trade relations with the United States continues to weigh on the automotive sector.

“It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.”

— Robert Kiyosaki

Key Upcoming Events

- In the United States, June inflation data will be released 07/14

- In the United States, June PPI will be released 07/15

Monitor:

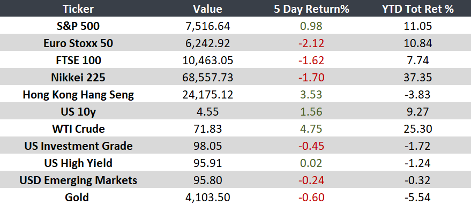

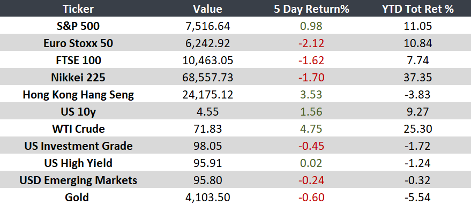

Note: Returns as of 10 AM ET