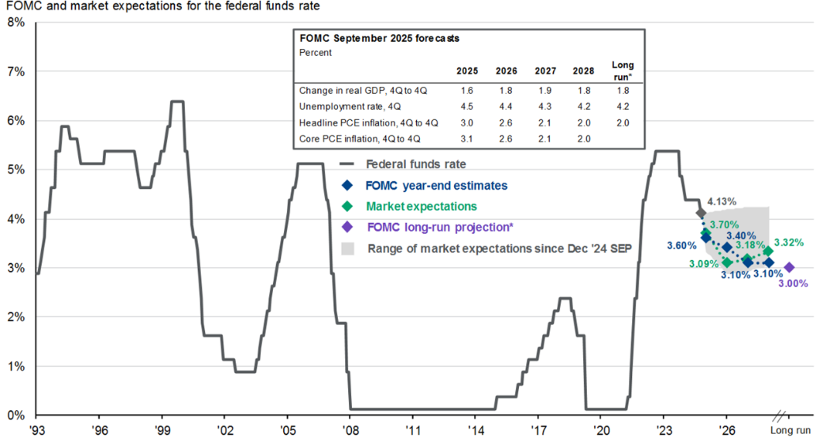

The Federal Reserve delivered its second rate cut of the year, lowering the policy rate by 25 bps to a range of 3.75%–4%. It announced that it will halt its balance sheet reduction in December.

The Fed acknowledged moderate growth but warned of rising labor market risks. The vote was 10–2, reflecting divided positions.

Powell: another cut in December is not guaranteed.

Key Data:

- Second rate cut of 2025

- Rate range: 3.75%–4%

- Vote: 10–2

- Balance sheet runoff to end in December

- Labor market risks on the rise

The market continues to expect a possible third rate cut in December, though signals remain mixed.

The Fed remains cautious and data-dependent, with employment as a key variable guiding the rate path.