September 8–12

U.S. inflation came in above expectations, but declines in producer prices and weak employment data reinforced expectations of a rate cut. In Latin America, Mexico and Brazil outlined new fiscal plans, while Europe and China continue to show trade fragility.

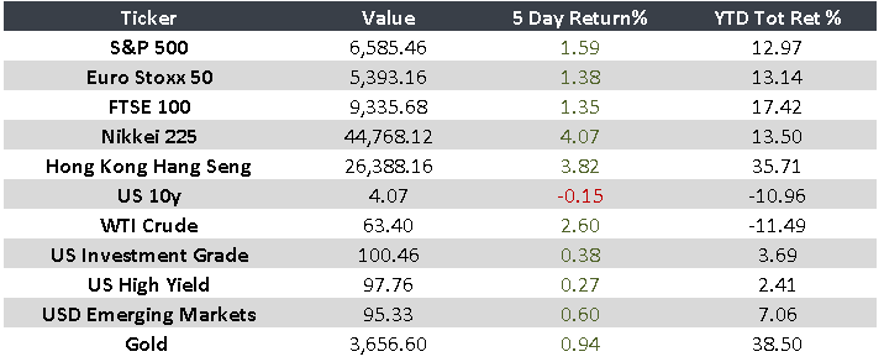

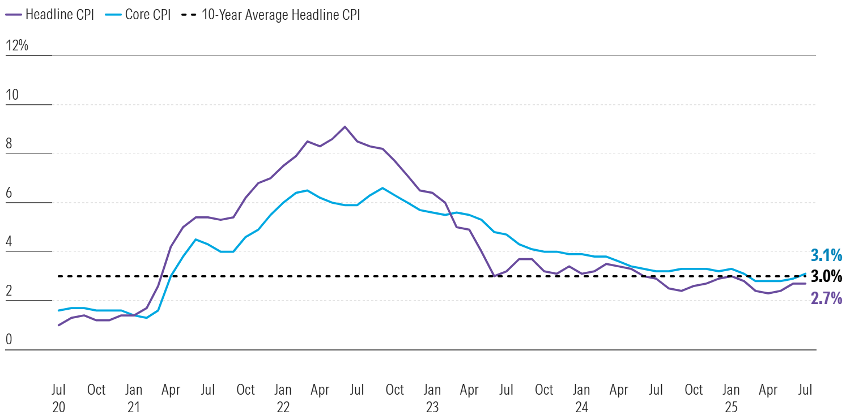

- United States: Inflation rose 0.4% in August, but the PPI fell 0.1%, reinforcing expectations of a rate cut. Together with weak employment data, this has fueled anticipation of the first cut since last year.

- Europe: German exports fell 0.6% month-over-month, including an 8% drop to the U.S. The ECB kept rates unchanged, while France faces new political challenges with the appointment of a new prime minister.

- China: Exports rose 4.4% year-over-year, below the 5% forecast. Inflation fell -0.4% YoY, while producer prices dropped 2.9% YoY, deepening the disinflationary trend.

- Japan: Q2 GDP was revised upward to 2.2% annualized, driven by stronger private consumption and inventory buildup.

- Brazil: Inflation eased to 5.13% YoY. While headline prices declined 0.11% MoM, services remain under pressure.

- Mexico: The 2026 economic package projects a lower deficit (4.16% of GDP) and growth between 1.8% and 2.8%. Pemex will receive $14 billion in support, and new tariffs on Chinese vehicles are under consideration.

“Time is your friend; impulse is your enemy.” — John C. Bogle

Key Events:

- U.S. Retail Sales — 09/16

- U.S. Monetary Policy Announcement — 09/18

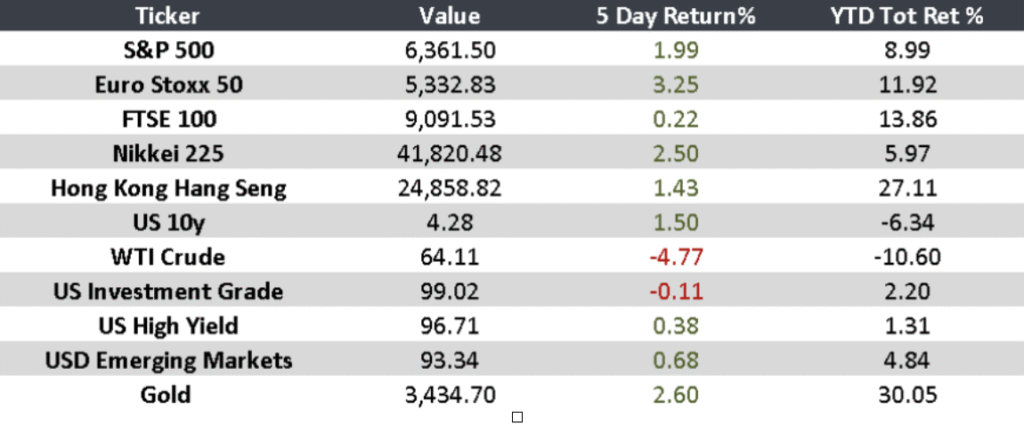

Monitor