PIK exposure remains stable at 6.6%, reflecting the structural flexibility characteristic of private credit. The portfolio maintains a meaningful allocation to software, historically the sector with the lowest default rates due to high margins, low capex, and recurring revenue.

PIK and structural flexibility

Liquid (traded) loans should not have PIKs. PE sponsors seek capital flexibility and access — that’s a key value driver of private credit.

PIK is a form of flexibility — more common in private credit, not applicable in public markets. Bain, for example, does not offer PIK flexibility — they lend to significantly smaller businesses than BCRED’s target market.

PIK is a form of flexibility — reserved for private credit, absent in public markets. Bain: no PIKs, but their borrowers are significantly smaller than BCRED’s portfolio companies.

Software as a defensive sector

Software: historically the lowest default sector in private credit — driven by low capex, high margins, and recurring revenue. Attractive sector for capital deployment.

98% first lien. Focus on scale businesses: ~$360mm average EBITDA. ~$4bn average total enterprise value per portfolio company. Healthy businesses.

Lowest default sector over the past 20 years — key rationale for the overweight.

Artificial intelligence risk

On AI risk to software: Jensen Huang’s view — people will be more efficient, but enterprises won’t rebuild core software in-house. AI is a tool, not a replacement for existing software companies that hold patents and deep integrations (e.g., no one is rebuilding Dropbox).

Underwriting process: before any investment, Blackstone’s tech team (based in Miami) evaluates the business, and then consults multiple Blackstone PE teams — if the PE teams would not invest in the equity, Blackstone will not lend to the company.

Largest software positions include cybersecurity. Not all software is the same — Blackstone categorizes by AI exposure and risk profile.

Of the ~26% software allocation, only ~5% is considered at risk from AI disruption. Meaningful headwinds identified; currently marked at ~88 cents on the dollar.

Worst-case scenario (100% default, recovery at 75 cents on the dollar): ~30bps drawdown to NAV.

Liquidity and maturities

Average remaining loan maturity: 3–5 years (~4 years average). Contract lengths align with loan maturities — provides visibility into repayment.

12–15% of the loan book matures this year; capital is also being deployed, maintaining strong liquidity. New capital being deployed in parallel — active recycling. A lot of liquidity.

Currently underlevered; target is 1:1 leverage ratio.

BCRED holds the highest credit rating of any private credit fund globally.

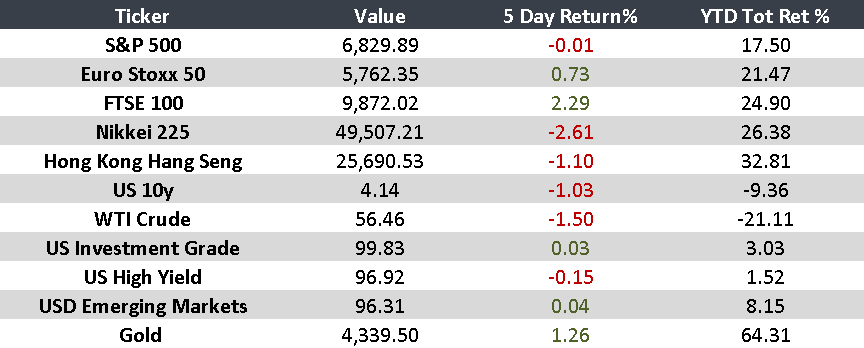

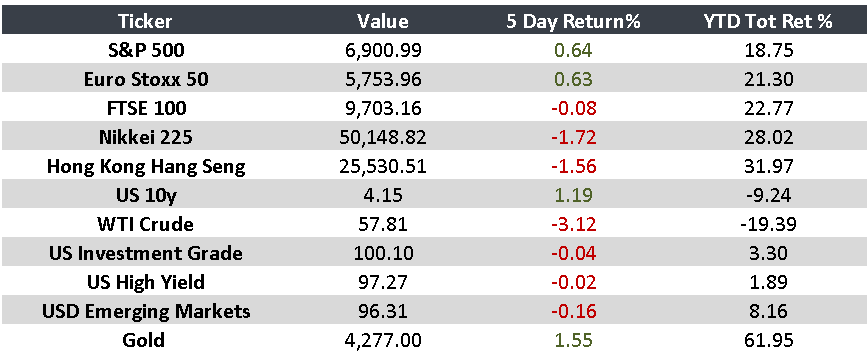

Source: Internal Research AWM