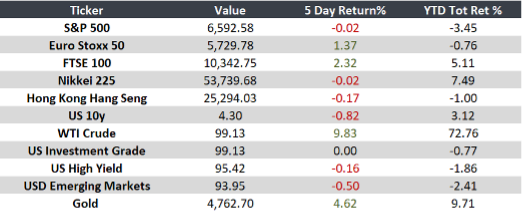

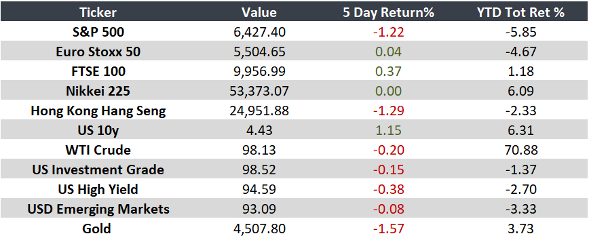

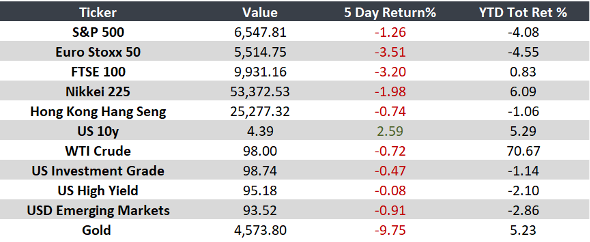

Week of April 13–17

Lower volatility, persistent inflation, and mixed growth signals shaped the week.

Markets experienced lower volatility amid expectations of easing geopolitical tensions. However, inflationary pressures persist alongside mixed growth signals across both developed and emerging economies.

United States

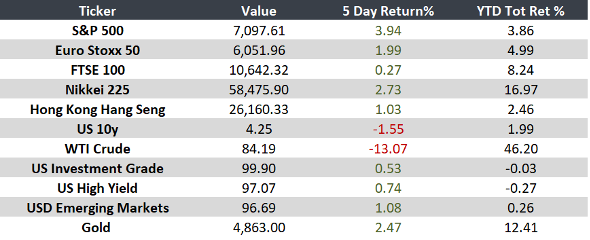

Lower volatility and the S&P 500 reached record highs. Moderate producer inflation and a resilient labor market support a growth environment with contained pressures.

Europe

Inflation rises due to energy, while industrial activity remains weak. The UK stands out with growth driven by services and construction.

Japan

Production grows marginally, and the BoJ may accelerate rate hikes. Slower growth is expected in the coming years.

China

Solid GDP growth, but mixed signals in consumption and employment point to an uneven recovery.

Argentina

Inflation remains elevated despite slight moderation, reflecting ongoing macroeconomic pressures.

Brazil

Consumption slows and industrial confidence declines, signaling deterioration in economic activity.

Mexico

Inflation pressures lead to price control measures. Trade risks rise amid potential changes to USMCA rules.

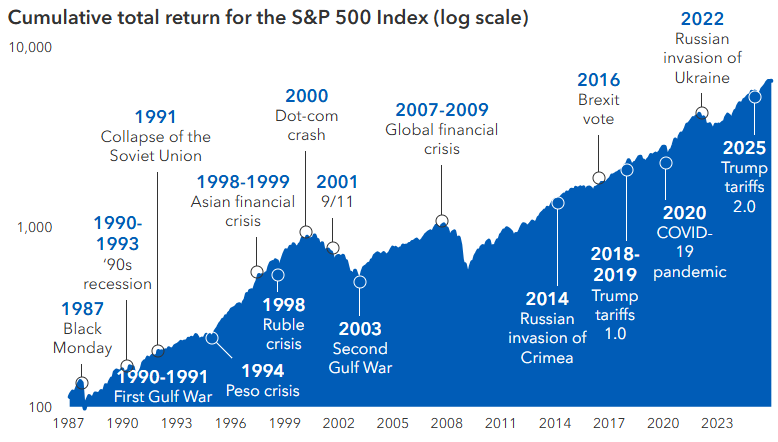

“Patience is not passive; it is concentrated strength.” – Bruce Lee

Key upcoming events

- Retail sales data to be released on April 21

- Employment-related data to be released on April 23

Monitor