Week of May 18 to May 22

A week marked by inflation pressures, rising rates, and mixed growth signals

Markets are facing a more restrictive environment, with persistent inflationary pressures and rising interest rates. While some economies show resilience, others reflect a slowdown, amid ongoing geopolitical risks.

United States

- Fed Minutes point to potential rate hikes.

- 30-year yields surpass 5%.

- Earnings grow ~28%, but housing weakens.

- Labor market remains resilient.

Europe

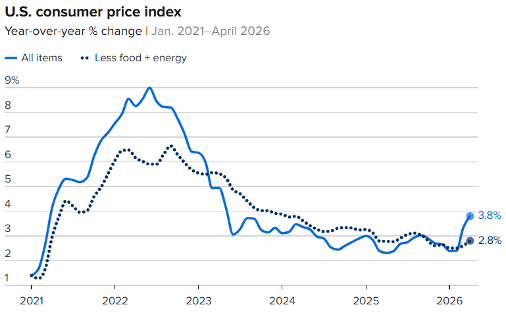

- Eurozone inflation rises to 3.0% driven by energy.

- UK inflation moderates, but unemployment increases.

- Germany grows in line with expectations, with rising cost pressures.

Japan

- GDP exceeds expectations, but energy costs threaten growth.

- Inflation falls to 1.4%, remaining below the central bank’s target.

China

- Retail sales and industrial production slow.

- Weak domestic demand reflects softer consumption and manufacturing momentum.

Argentina

- Economic activity rebounds to 5.5%, reversing the previous contraction and signaling recovery.

Brazil

- Economic activity declines monthly but maintains 3.1% annual growth, reflecting partial resilience.

Mexico

- Moody’s downgrades rating to Baa3.

- Growth remains moderate, supported by services and easing inflation.

“Be fearful when others are greedy. Be greedy when others are fearful.” — Warren Buffett

KEY UPCOMING EVENTS

- In the United States, markets will remain closed for Memorial Day 05/25

- In the United States, employment related data will be released 05/27

Monitor:

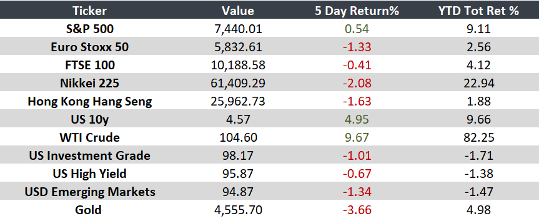

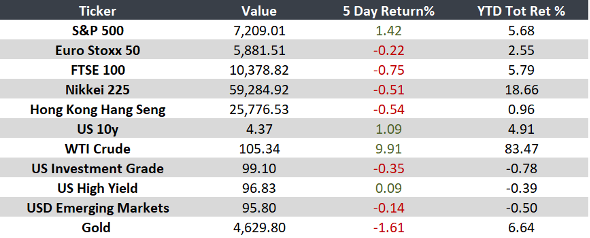

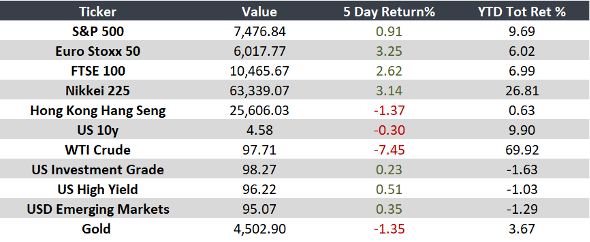

Note: Returns as of 10 AM ET.

Source: JP Morgan