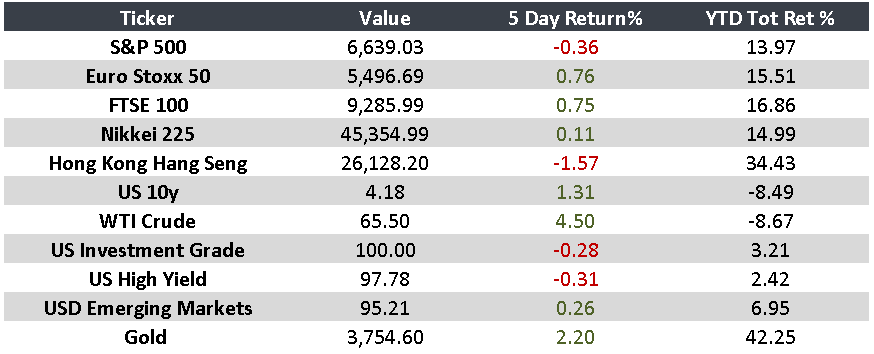

September 22–26

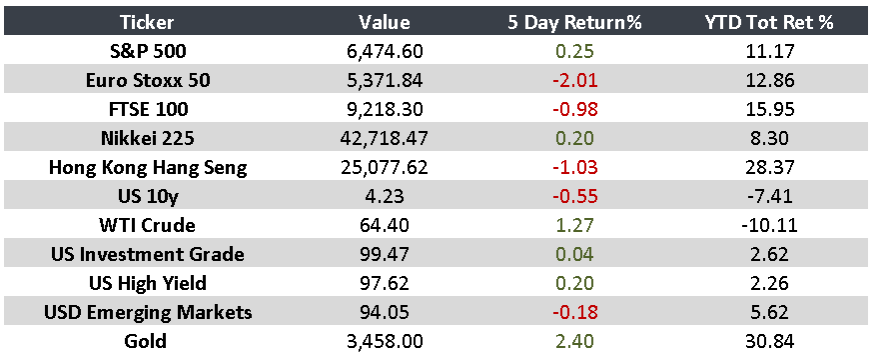

General Summary: In an environment marked by monetary uncertainty and resilient consumption, the latest data and comments from financial authorities show a mixed picture: while the OECD revised global growth forecasts upward, some central banks remain cautious and highlight medium-term risks.

United States

- Fed Governor Stephen Miran stated that interest rates are too high and should be cut by up to 200 bps.

- Jerome Powell warned that equity valuations remain elevated and the path to rate cuts is uncertain.

- Q2 GDP was revised upward to 3.8% annualized, supported by consumer spending.

- OECD projects global growth of 3.2% in 2024 and 1.8% for the U.S. in 2025.

Europe

- UK retail sales rose 0.5% in August.

- Eurozone business activity reached its fastest pace in 16 months, led by Germany’s service sector.

- The Swiss National Bank held rates at 0% and warned about the potential impact of U.S. tariffs through 2026.

Japan

- Manufacturing contracted at the sharpest pace in six months.

- The services producer price index rose 2.7% YoY in August.

China

- Donald Trump advanced plans for U.S. investors to acquire TikTok’s U.S. operations from ByteDance, valued at $14 billion.

Mexico

- Banxico cut the policy rate to 7.5%, the lowest level in three years.

- Inflation in the first half of September stood at 3.74% YoY, in line with expectations.

- OECD revised growth to 0.8% in 2024 (from 0.4%) and to 1.3% in 2026 (from 1.1%).

“The greatest enemy of a good plan is the dream of a perfect plan. Stick to the good plan.” — John C. Bogle

Key Events:

- U.S.: Consumer Confidence — September 30

- U.S.: Employment Report — October 03

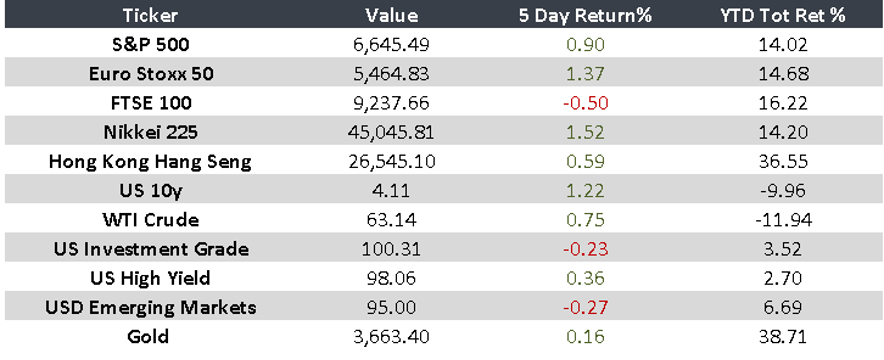

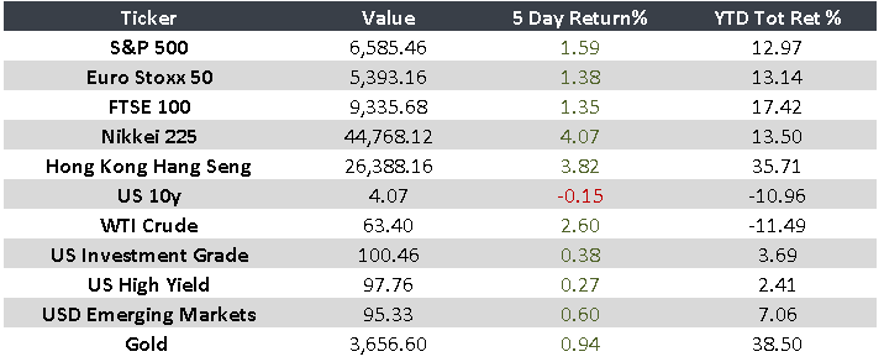

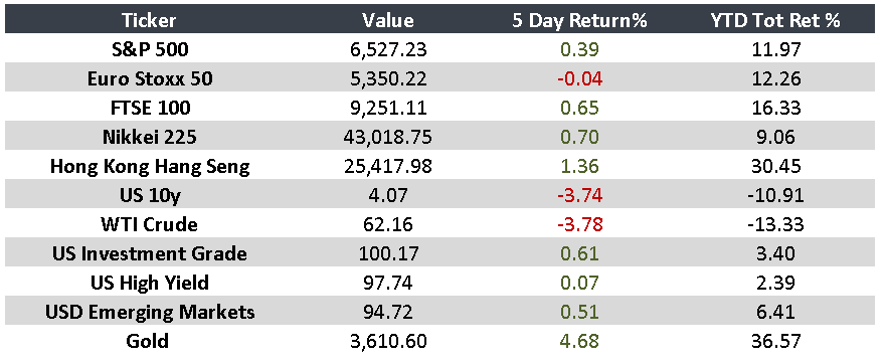

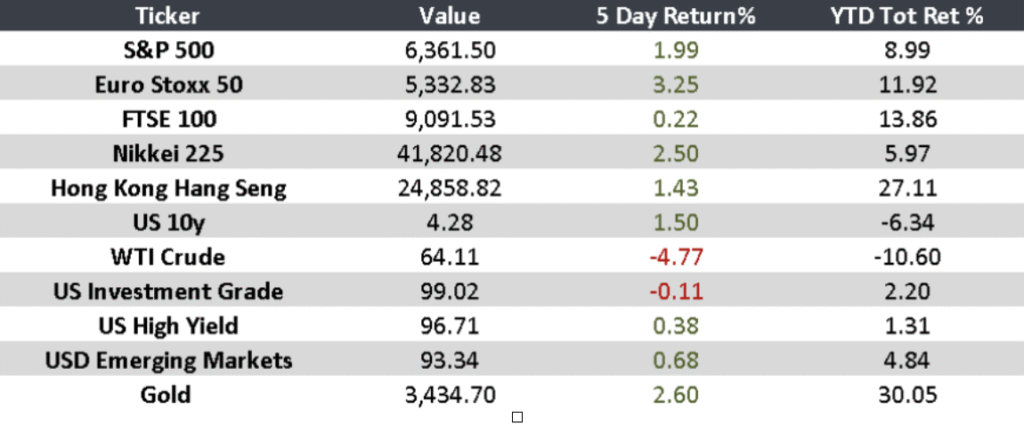

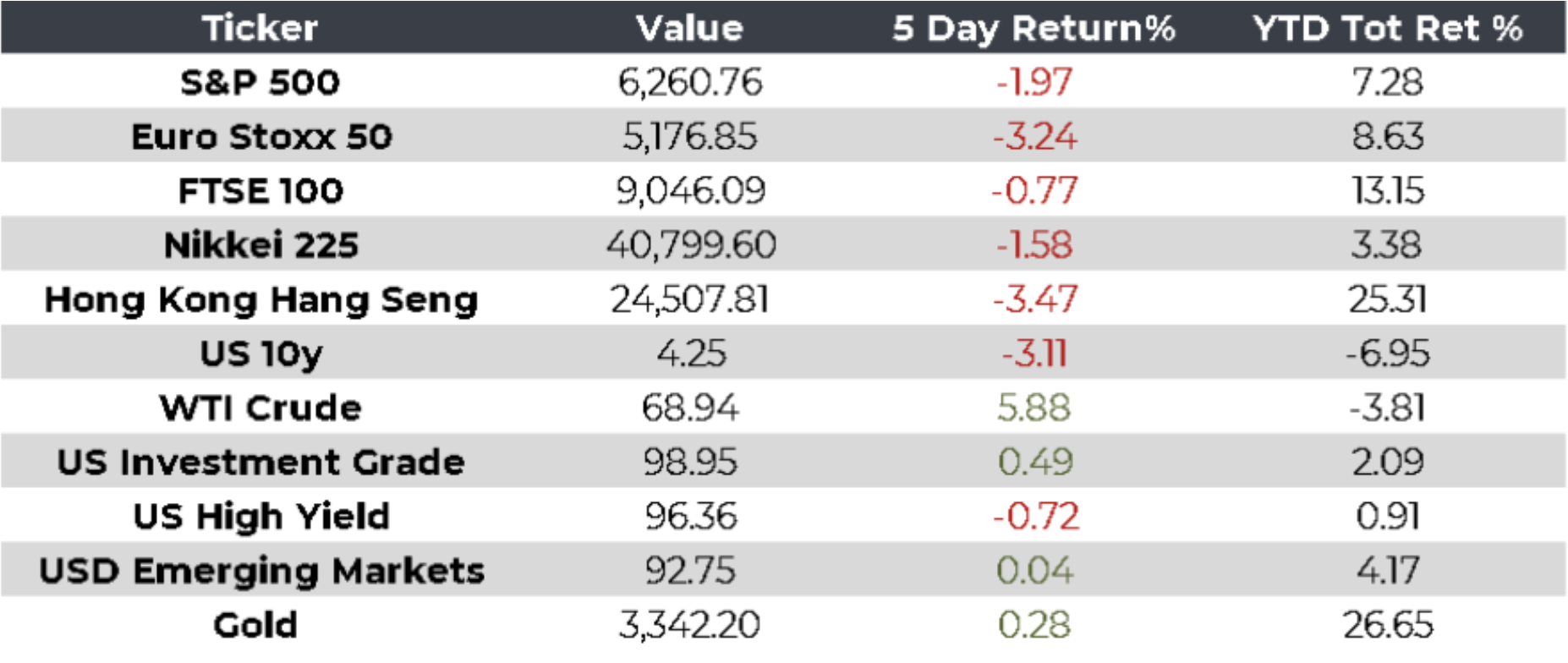

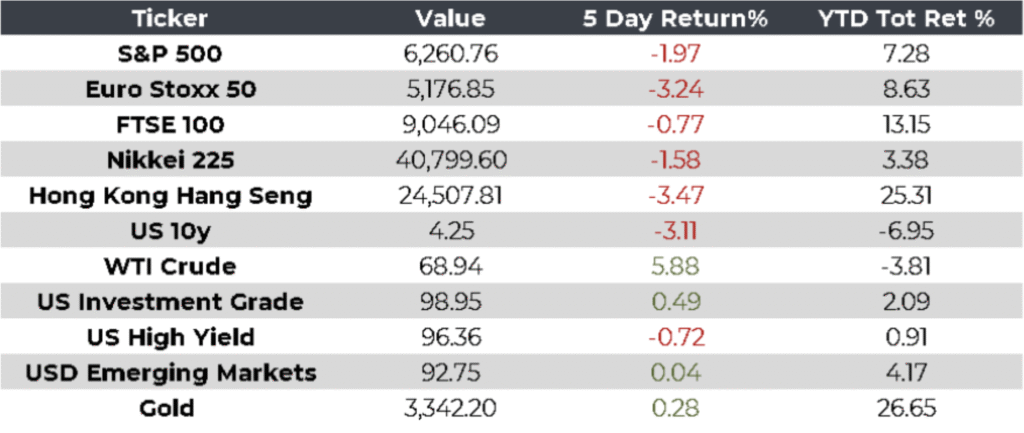

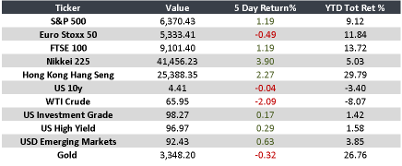

Monitor